You’ve got $10,000 — maybe from savings, a bonus, or a windfall — and you’re wondering what it could become if you simply left it to grow. It’s one of the most motivating questions in personal finance, because the answer reveals just how powerful patience and compounding really are. Let’s run the numbers.

The short answer

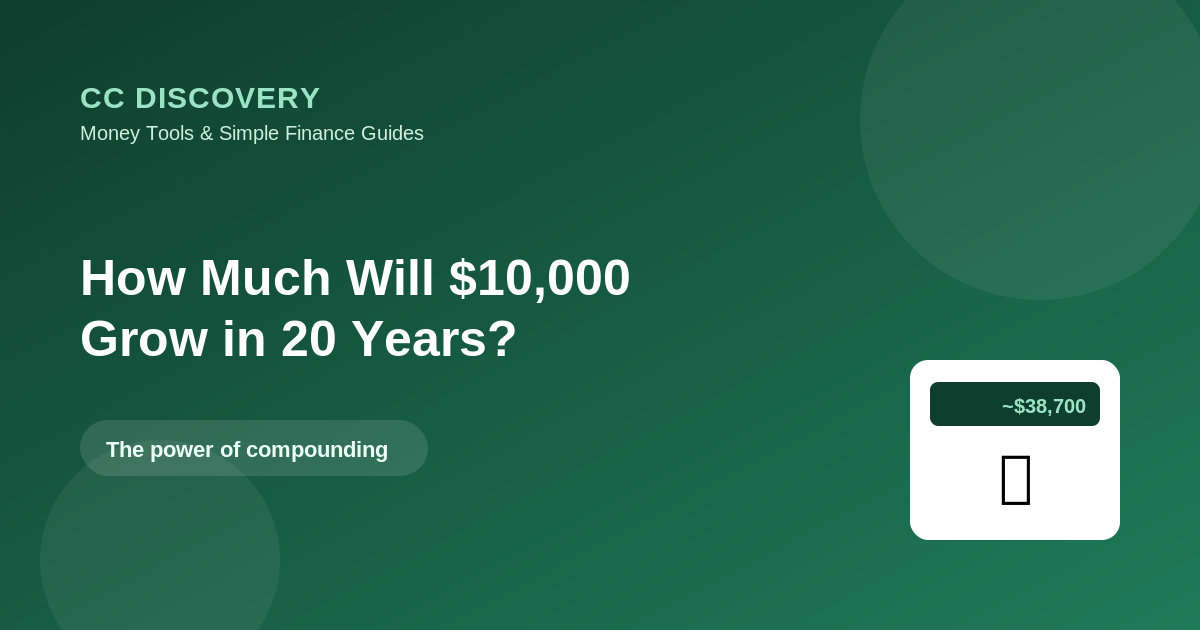

It depends entirely on the rate of return. Left untouched for 20 years, a single $10,000 deposit grows to roughly:

| Annual return | $10,000 after 20 years |

|---|---|

| 4% (high-yield savings / bonds) | ~$21,900 |

| 7% (long-run stock market average) | ~$38,700 |

| 10% (higher-risk, optimistic) | ~$67,300 |

At a 7% average return — roughly what a broad stock-market index has delivered over the long run before inflation — your $10,000 nearly quadruples without you adding a single extra dollar. Try your own numbers and timeline in the Compound Interest Calculator.

Why the rate matters so much

Look at that table again. The difference between 4% and 7% isn’t small — it’s about $17,000 over 20 years on the same starting amount. That gap is why where you put money matters as much as whether you save it. Cash sitting in a near-0% account barely grows (and loses ground to inflation), while the same money in diversified, long-term investments can multiply.

This is the engine of compounding: each year you earn returns not just on your original $10,000, but on all the growth that came before it. The snowball gets bigger as it rolls.

The magic of adding to it

Leaving $10,000 alone is impressive. Adding to it is transformational. Suppose you keep that $10,000 and add $200 a month for 20 years at a 7% return:

- You’d contribute: $10,000 + $48,000 = $58,000

- It would grow to: about $137,000

More than half of that final balance is growth you never deposited. The lesson: a lump sum is a great start, but regular contributions are what build real wealth. See it for yourself in the Compound Interest Calculator.

The catch: returns aren’t smooth

A 7% average doesn’t mean 7% every year. Real markets rise and fall — some years up 20%, some down 15%. The long-term averages only show up for people who stay invested through the dips instead of panic-selling. The U.S. SEC’s investor site, Investor.gov, is a solid, no-hype place to learn more.

And inflation quietly nibbles at returns over time, which is exactly why beating inflation — rather than leaving cash idle — is the whole point of long-term investing.

Where might $10,000 grow?

This article is about the math, not specific recommendations, but in general:

- Safe and steady (lower growth): high-yield savings, CDs, bonds.

- Long-term growth (more risk): diversified investments like index funds, often held in tax-advantaged accounts like a Roth IRA or 401(k).

The right mix depends on your timeline and comfort with risk. Money you need soon should stay safe; money you won’t touch for 20 years has time to ride out the ups and downs.

Frequently asked questions

How much will $10,000 grow in 20 years?

At a 7% average return, about $38,700 if left untouched. At 4%, about $21,900; at 10%, about $67,300.

Is 7% a realistic return?

It’s roughly the long-run historical average of a broad stock-market index before inflation — but it’s an average, not a guarantee, and individual years vary widely.

Will I really quadruple my money?

At ~7% over 20 years, yes, the math works out to nearly 4x — but only if you stay invested and don’t withdraw early.

Should I add monthly contributions?

If you can, absolutely. Regular contributions dwarf a one-time lump sum over long periods, as the $137,000 example shows.

The takeaway

Left alone for 20 years, $10,000 grows to roughly $38,700 at a 7% average return — nearly quadrupling on its own. Add steady monthly contributions and the same start can become six figures. The keys are time, a return that beats inflation, and the patience to stay invested. Model your exact scenario in the Compound Interest Calculator.

General educational information, not investment advice. All investing carries risk, including loss of principal.

Leave a comment