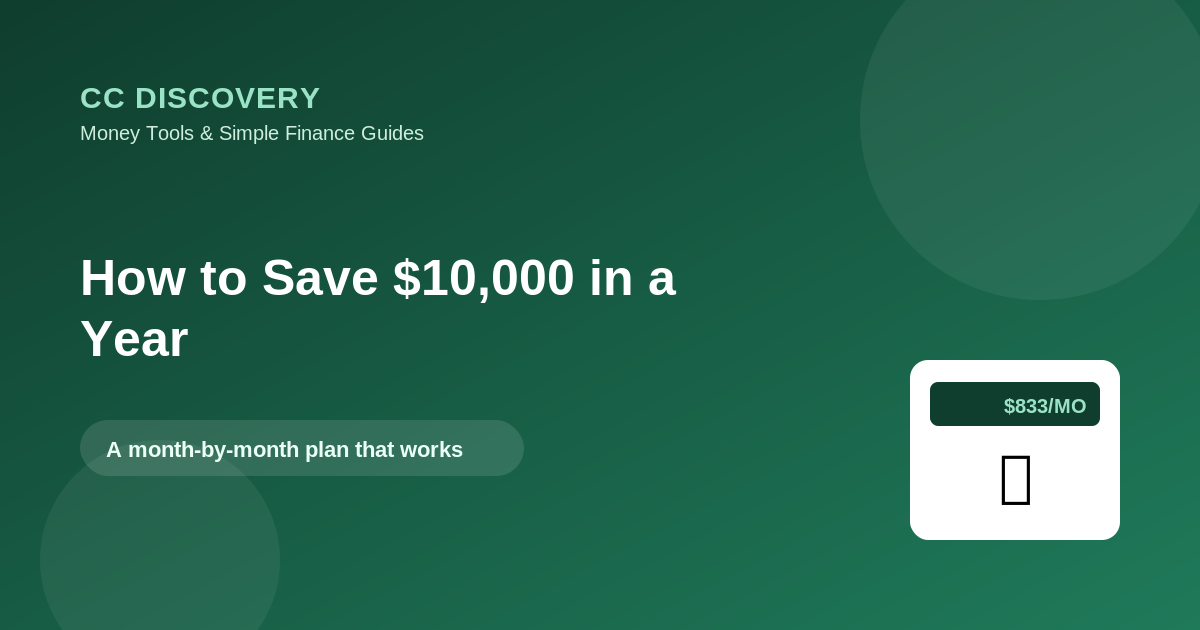

Ten thousand dollars in a year sounds like a stretch goal — the kind of thing only people with big salaries pull off. But broken down, it’s a math problem, not a miracle. It’s about $833 a month or roughly $192 a week. Once you see it that way, the question stops being “is this possible?” and becomes “where does the $833 come from?” Here’s a real plan to get there.

The target, broken down

Saving $10,000 in 12 months means:

| Timeframe | Amount to save |

|---|---|

| Per month | ~$833 |

| Per week | ~$192 |

| Per day | ~$27 |

Seeing the daily number can actually help — $27 is a number you can influence with everyday choices, not just big ones. To map out the timeline and adjust for any head start you have, use the Savings Goal Calculator.

Step 1: Find the money in your budget

Start by seeing where your money actually goes. Run your take-home pay through the 50/30/20 Budget Calculator, then hunt in two places:

- The “wants” bucket: dining out, subscriptions, impulse buys, upgrades you don’t need this year.

- Recurring “needs” you can lower: a cheaper phone or insurance plan, a refinanced bill, meal planning instead of last-minute takeout.

Most people can find $300–500 a month here without feeling deprived — they just have to look on purpose.

Step 2: Close the gap with income

If trimming gets you partway, income covers the rest. You don’t need a second full-time job — even an extra $200–400 a month from a side gig, selling unused items, overtime, or a freelance skill can bridge the difference. Combine $500 in cuts with $333 in extra income and you’ve hit $833 without gutting your lifestyle.

Step 3: Automate it so it actually happens

Willpower fades; automation doesn’t. Set up an automatic transfer of your target amount into a separate high-yield savings account the day after each payday — before you can spend it. Money you never see in checking is money you don’t miss. This single habit does more than any budgeting app.

A sample month-by-month approach

You don’t have to save exactly $833 every month — you smooth it around your life:

- Months with a bonus, tax refund, or extra paycheck: save more (catch-up months).

- Tight months (holidays, a big bill): save a little less, and make it up later.

- Use windfalls fully: a tax refund of $2,000 thrown straight in covers nearly three months of the goal at once.

The target is the year-end total, so a few uneven months are fine as long as the average holds.

Step 4: Protect the money

Two rules keep your $10,000 from leaking away:

1. Keep it separate. A dedicated savings account (ideally at a different bank) makes it harder to dip into.

2. Earn interest while it sits. A high-yield savings account pays you a little extra and keeps the money safe and reachable — important if this is also your emergency fund.

What to do with the $10,000

Decide the purpose before you start — it keeps you motivated. Common goals: a fully funded emergency fund, a house down payment, paying off high-interest debt (see the Credit Card Payoff Calculator), or seed money for investing, where compound interest can grow it for decades.

Frequently asked questions

How much do I need to save per month to reach $10,000 in a year?

About $833 a month, or roughly $192 a week. A head start or a bigger return lowers the monthly amount slightly.

What if I can’t save $833 every month?

Save what you can and use catch-up months (bonuses, refunds, extra paychecks). The goal is the year-end total, not a perfect monthly streak.

Where should I keep the money?

A separate high-yield savings account — safe, earning interest, and harder to spend impulsively.

Is saving $10,000 in a year realistic?

For many people, yes — by combining $300–500 in budget cuts with some extra income, and automating the transfer.

The takeaway

Saving $10,000 in a year is just $833 a month — found through a mix of budget cuts and a little extra income, then automated into a separate high-yield account before you can spend it. Set your number and timeline with the Savings Goal Calculator, free up the cash with the 50/30/20 Budget Calculator, and let consistency do the rest.

General educational information, not financial advice.

Leave a comment