The first time I filed taxes with freelance income, one line on the return stopped me cold: self-employment tax. I’d budgeted for income tax, but this was a whole extra chunk I didn’t see coming. If you earn money working for yourself — freelancing, gig work, a side business — this is the tax most likely to surprise you. So let’s demystify it: what it is, how much it costs, and how to plan for it.

What self-employment tax actually is

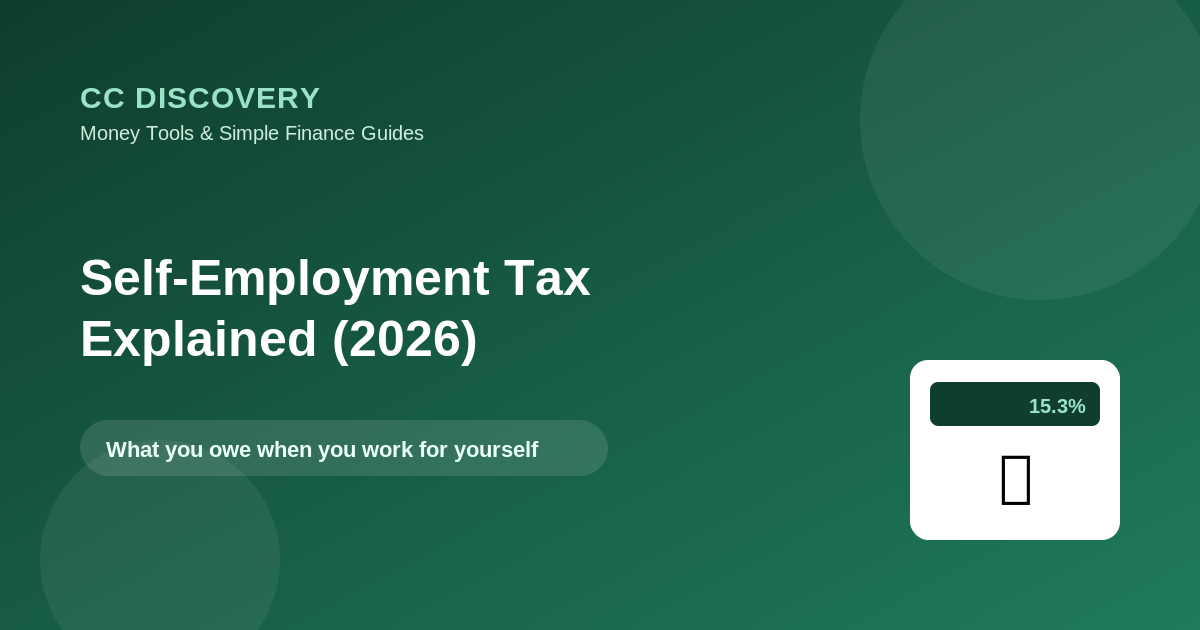

When you have a regular job, Social Security and Medicare taxes (together called FICA) are split between you and your employer — you each pay 7.65%. When you work for yourself, you are both the employee and the employer, so you pay both halves. That combined amount is “self-employment tax.”

It is separate from income tax. You pay self-employment tax and income tax on your self-employment earnings.

The rate: 15.3%

Self-employment tax is 15.3% of your net self-employment earnings, broken down as:

| Component | Rate | Applies to |

|---|---|---|

| Social Security | 12.4% | Net SE earnings up to the wage base ($184,500 in 2026) |

| Medicare | 2.9% | All net SE earnings (no cap) |

| Total | 15.3% |

High earners also pay an extra 0.9% Additional Medicare Tax on earnings above $200,000. The IRS explains the details at irs.gov.

Two things that soften the blow

The 15.3% sounds brutal, but two rules make it less painful than it first appears:

1. It’s applied to 92.35% of your net earnings, not 100%. You multiply your net self-employment profit by 0.9235 before the 15.3%.

2. Half of it is deductible. You can deduct the “employer half” of the tax from your income before calculating income tax. It doesn’t reduce the SE tax itself, but it lowers your income-tax bill.

A quick example

Say you have $50,000 in net self-employment profit (after business expenses):

- Taxable base: $50,000 times 0.9235 = $46,175

- Self-employment tax: $46,175 times 15.3% = about $7,065

- You can then deduct about $3,533 (half) when figuring your income tax.

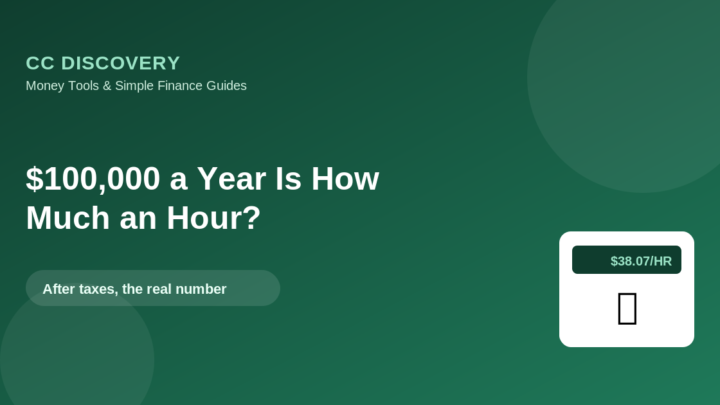

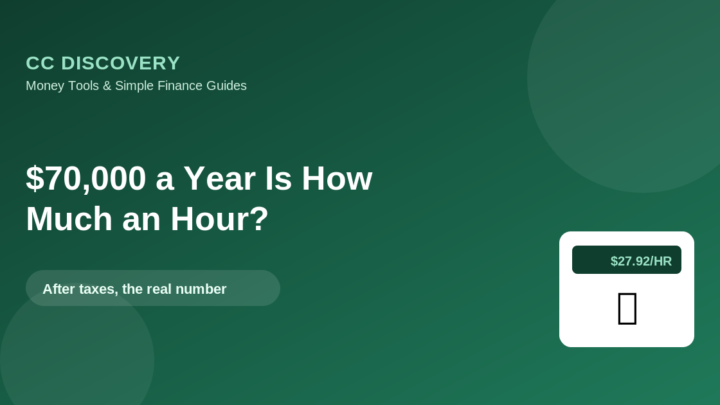

On top of that ~$7,065, you’ll also owe regular income tax on your profit — estimate that piece with the Income Tax Estimator.

Why business expenses matter so much

Self-employment tax is charged on your net profit — revenue minus legitimate business expenses. That makes tracking deductible costs (home office, equipment, software, mileage, supplies) genuinely valuable: every dollar of legitimate expense lowers both your self-employment tax and your income tax. Good record-keeping is one of the most effective ways a freelancer reduces their bill.

How to plan for it (so it’s not a shock)

Because nobody withholds this for you, you handle it yourself:

- Set aside 25–30% of every payment into a separate tax account. This typically covers self-employment tax plus income tax.

- Pay quarterly estimated taxes so you don’t owe it all at once — and avoid a penalty. See How to Pay Quarterly Estimated Taxes.

- Track expenses all year, not just at tax time.

This is the core difference between contractor and employee pay we cover in W-2 vs 1099.

Frequently asked questions

Do I owe self-employment tax on a small side hustle?

Generally, if your net self-employment earnings are $400 or more, you owe self-employment tax — even on a small side gig.

Is self-employment tax the same as income tax?

No. They’re separate. Self-employment tax covers Social Security and Medicare; income tax is calculated on your taxable income. You pay both on self-employment profit.

Can I lower my self-employment tax?

Yes — by deducting all legitimate business expenses (which lowers net profit) and keeping good records. Some business structures can also affect it, which is worth discussing with a tax pro.

Does the deduction cancel out the tax?

No. The “half is deductible” rule only reduces your income tax, not the self-employment tax itself.

The takeaway

Self-employment tax is the 15.3% you pay for Social Security and Medicare when you work for yourself — both the employee and employer halves. It applies to about 92% of your net profit, half is deductible against income tax, and good expense tracking shrinks it. Plan ahead: set aside ~25–30% of every payment, pay quarterly estimated taxes, and estimate your income-tax piece with the Income Tax Estimator.

General educational information for 2026, not tax advice. Consult a qualified tax professional about your situation.

Leave a comment