When you sit down to choose a mortgage, the lender hands you two doors: 15 years or 30 years. The 30-year has the smaller, friendlier monthly payment, so most buyers walk through it without much thought. But that smaller payment hides a much bigger lifetime price tag. Let’s put both side by side with real numbers so you can choose on purpose, not by default.

The core trade-off

It comes down to one tension:

- 30-year mortgage: lower monthly payment, but you pay interest for twice as long — so the total cost is far higher.

- 15-year mortgage: higher monthly payment, but you’re debt-free in half the time and save a fortune in interest. Lenders also usually offer a slightly lower interest rate on 15-year loans.

Neither is “wrong.” They serve different priorities: monthly breathing room versus long-term savings.

A real example: a $300,000 loan

Say you borrow $300,000. Here’s how the two stack up (using typical rates):

| 30-year @ 6.5% | 15-year @ 5.8% | |

|---|---|---|

| Monthly payment (P&I) | ~$1,896 | ~$2,499 |

| Total interest paid | ~$382,600 | ~$149,900 |

| Total paid | ~$682,600 | ~$449,900 |

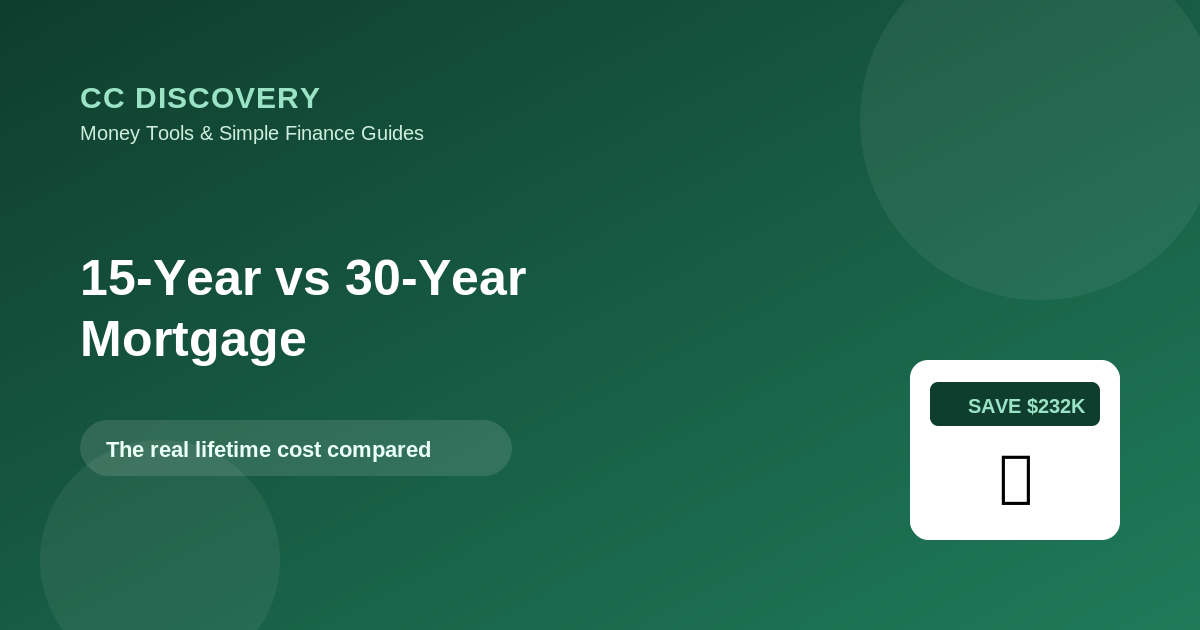

The 15-year costs about $603 more per month — but saves roughly $232,700 in interest over the life of the loan. That’s the real headline: the cheaper monthly payment on the 30-year quietly costs you nearly a quarter-million dollars more. Run your own loan amount through the Mortgage Calculator to see your numbers.

Why the 15-year saves so much

Two forces stack up in its favor:

1. Less time accruing interest. You’re borrowing for 180 months instead of 360, so interest has half as long to pile up.

2. A lower rate. Lenders typically price 15-year loans a bit cheaper because they get their money back faster.

Together, those can cut total interest by more than half.

Why people still choose the 30-year

The 30-year isn’t a trap — it’s the right call for many buyers:

- Lower required payment means more monthly flexibility for saving, investing, or simply affording the home.

- You can pay it like a 15-year voluntarily. Take a 30-year loan but make extra principal payments when you can. You get the lower required payment as a safety net, with the freedom to pay down faster in good months.

- Opportunity cost: if you can earn more by investing the ~$600/month difference than you’d save in mortgage interest, the 30-year plus investing can come out ahead — though that’s not guaranteed.

How to decide

Ask yourself: Can I comfortably afford the 15-year payment and still save and invest? If yes, it’s a powerful wealth move. Would the higher payment leave me stretched with no emergency fund? Then the 30-year’s flexibility is safer — and you can still pay extra when possible.

A middle path many people love: take the 30-year, but add extra principal toward it. Even one extra payment a year shaves years off the loan. The U.S. Consumer Financial Protection Bureau has neutral guides on comparing loan terms at consumerfinance.gov.

Frequently asked questions

Is a 15-year mortgage worth it?

If you can comfortably afford the higher payment, yes — it can save well over $200,000 in interest on a typical loan and makes you debt-free in half the time.

Why is the 15-year payment so much higher?

You’re repaying the same principal in half the time, so each payment is larger — even though the rate is usually lower.

Can I pay off a 30-year mortgage early?

Yes. Make extra principal payments anytime (most loans have no prepayment penalty) to cut years and interest. You keep the lower required payment as a backup.

Which has the lower interest rate?

15-year loans usually carry a slightly lower rate than 30-year loans.

The takeaway

The 30-year mortgage wins on monthly payment; the 15-year wins decisively on total cost — often saving more than $200,000 in interest and freeing you years sooner. Choose based on whether you can comfortably carry the higher payment while still saving. Either way, model both with the Mortgage Calculator, and remember you can take a 30-year and pay it down faster on your own terms.

General educational information, not financial advice. Rates vary — compare current offers with a licensed lender.

Leave a comment