Hitting a six-figure salary feels like a milestone — and it is. But “$100,000 a year” still has to survive a trip through the tax system before it becomes money you can actually spend. Let’s turn that big round number into the hourly and monthly figures you’d really plan your life around.

The quick math: $100,000 a year per hour

A full-time year is 40 hours a week times 52 weeks = 2,080 hours. So:

$100,000 divided by 2,080 = about $48.08 per hour (gross).

That’s the headline rate. Satisfying, but not what lands in your account.

After taxes: what you actually keep

For a single filer in 2026 with no state income tax, $100,000 breaks down roughly like this:

| Item | Amount (per year) |

|---|---|

| Gross salary | $100,000 |

| Federal income tax | about $13,170 |

| Social Security + Medicare (FICA) | about $7,650 |

| Take-home pay | about $79,180 |

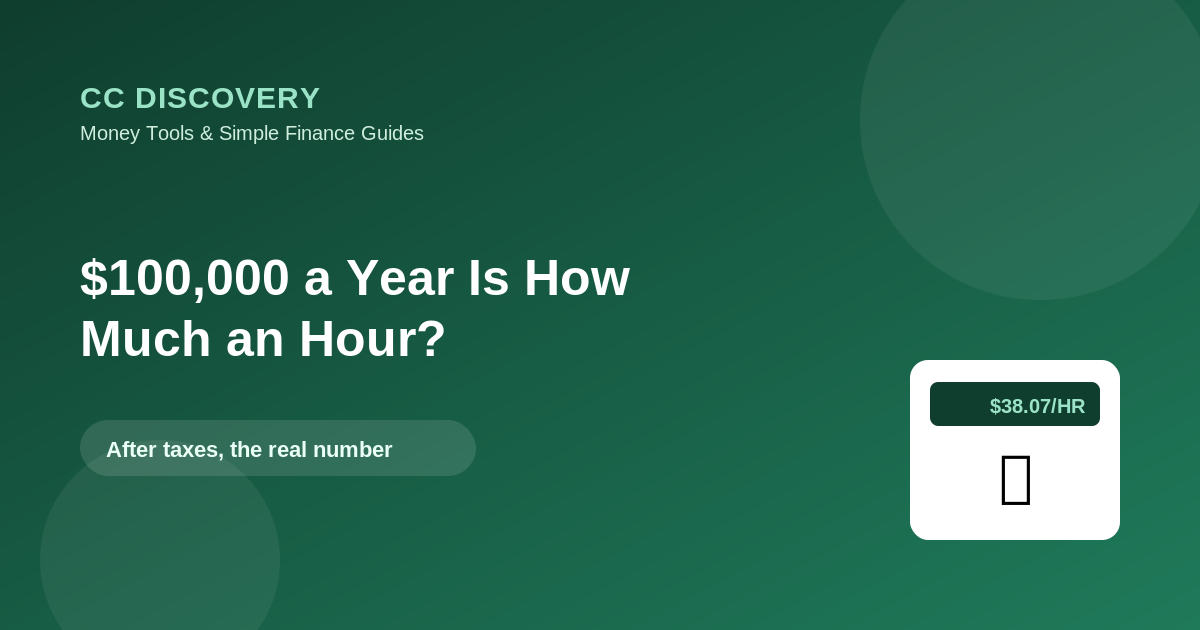

Divide the take-home by 2,080 hours and you keep about $38.07 per hour. So “$48/hour” on paper is really closer to $38/hour in spendable pay — and a state income tax would lower it further. Get your exact, state-specific number in the Take-Home Pay Calculator.

Why $48 becomes ~$38

- FICA (7.65%): about $7,650 — Social Security (6.2%) up to the 2026 wage base of $184,500, plus Medicare (1.45%) on everything.

- Federal income tax: about $13,170, calculated after the $16,100 standard deduction and progressively across brackets. Your top dollars reach the 22% bracket, but your effective federal rate is only about 13% — because the lower brackets tax the earlier dollars at 10% and 12%. See How Tax Brackets Really Work.

$100,000 in other useful terms

- Per hour (gross): ~$48.08

- Per hour (take-home): ~$38.07

- Per week (gross): ~$1,923

- Per month (gross): ~$8,333

- Per month (take-home): ~$6,598

- Per bi-weekly paycheck (take-home): ~$3,045

Single filer, no state tax, standard deduction. Add a state income tax and your real paycheck shrinks.

Is $100,000 a good salary?

In most of the country, six figures is a comfortable income — but in the most expensive metros it’s solidly middle-class, not lavish. The honest test is the same at every income: budget from take-home (~$6,598/month) using a 50/30/20 split — about $3,299 for needs, $1,979 for wants, and $1,320 for savings. At this income, that ~$1,300/month savings bucket is where real wealth gets built if you actually invest it.

Make six figures count

- Max your 401(k) match, then push contributions higher — it lowers your taxable income and compounds for decades. Try the Compound Interest Calculator.

- Avoid lifestyle creep. The fastest way to feel broke on $100k is to spend like you make $130k.

- Automate savings first so the 20% leaves before you can spend it.

Frequently asked questions

Is $100,000 a year $48 or $38 an hour?

About $48.08/hour gross, but roughly $38.07/hour in take-home pay for a single filer with no state tax.

How much is $100,000 a year monthly after taxes?

Around $6,598/month take-home (single, no state tax). A state income tax reduces it.

Why isn’t my whole salary taxed at 22%?

Because brackets are slices — only the income above each threshold is taxed at the higher rate. Your effective rate (~13% federal here) is far below your top bracket.

Does this include state tax?

No — federal only. Use the Take-Home Pay Calculator with your state for an exact figure.

The takeaway

“$100,000 a year” is about $48 an hour on paper and roughly $38 an hour after taxes for a single filer. Plan around the take-home (~$79,180/year, ~$6,598/month), automate aggressive savings, and watch lifestyle creep. Get your precise number with the Take-Home Pay Calculator, and compare with $70,000 a Year Is How Much an Hour.

General educational information for 2026, not tax advice. Estimates assume a single filer with no state income tax.

Leave a comment