Most saving advice is annoyingly vague. “Save more.” “Pay yourself first.” Sure — but how much? When I wanted to save for a down payment, what I actually needed was one number: the amount to move out of my account every month so I’d arrive on time. Not a vibe. A number.

That’s what this is. We’re going to work backward from the goal.

Start at the finish line, not the start

Instead of saving whatever’s left over and hoping it’s enough, you decide three things up front:

1. The goal — how much you need (say, $20,000 for a down payment).

2. The deadline — when you need it (say, 3 years).

3. What you’ve already saved — your starting point (say, $2,000).

From those, the required monthly amount is just math. The Savings Goal Calculator does it instantly, but understanding the logic helps you adjust when life changes.

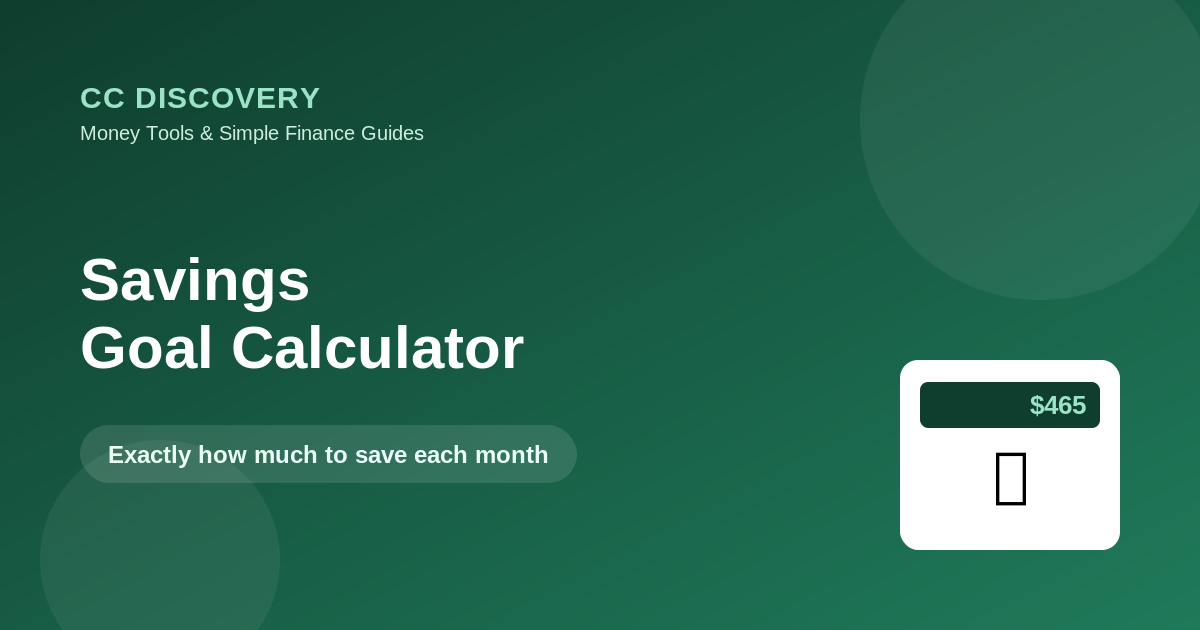

A real example: $20,000 in 3 years

You want $20,000, you’ve already got $2,000, you’ve got 36 months, and your savings earn about 4% a year in a high-yield account.

The calculator says: about $465 a month.

That’s the whole point — you’ve turned a fuzzy “I should save for a house” into a concrete “$465 leaves my checking account on the 1st.” And notice the 4% return is quietly helping: without any interest you’d need closer to $500/month, so the account is doing a little of the work for you.

What to do when the number feels too big

Run your real goal and you might get a monthly figure that makes you wince. Good — better to know now. You have four honest levers:

- Extend the deadline. Stretching 3 years to 4 drops the monthly amount a lot.

- Lower the goal. Maybe a 10% down payment instead of 20%, or a cheaper target.

- Boost the starting amount. A tax refund or bonus thrown in early reduces every future payment.

- Earn a better return. Moving cash to a high-yield savings account or, for long-term goals, investments, lowers the monthly burden — though investing adds risk.

Play with these in the calculator. Seeing the monthly number drop as you extend the timeline makes the trade-offs obvious.

Match the account to the timeline

One rule that saves people a lot of stress: the sooner you need the money, the safer it should be.

- Short-term goals (under ~3 years) — a high-yield savings account. You want the money to be there for certain, not riding the stock market.

- Long-term goals (5+ years) — investments can make sense, because you have time to ride out the ups and downs and let compound interest do more of the lifting.

The U.S. government’s MyMoney.gov has straightforward, ad-free guidance on saving if you want a second source.

Automate it or it won’t happen

Knowing your number is half the battle. The other half is making the transfer automatic. Set up a recurring transfer for the day after payday, into a separate savings account you don’t casually dip into. Money you never see in your checking account is money you don’t accidentally spend.

Frequently asked questions

What if my income is irregular?

Base your monthly target on a conservative income estimate, and “catch up” with extra in the good months. The calculator gives you the baseline to aim for.

Should I save or pay off debt first?

Usually: build a small emergency cushion, then attack high-interest debt (like credit cards) aggressively, then return to longer-term goals. High-interest debt grows faster than most savings, so the Credit Card Payoff Calculator is worth a look first.

Does the calculator account for interest?

Yes — enter an expected annual return and it factors in the growth, lowering the monthly amount you need.

The takeaway

Saving works when it’s a number, not a hope. Decide the goal, the deadline, and your starting point, then let the Savings Goal Calculator hand you the monthly figure. Automate that transfer, keep it in a separate account, and the goal mostly takes care of itself.

General educational information, not financial advice.

Leave a comment